It’s been one week since the new Trump administration has taken office, and from dozens of firsthand conversations, I can confidently say: this time feels different—there’s an overwhelming sense of instability on all fronts. On a national level, we’re grappling with massive macroeconomic uncertainty—tariffs, unemployment concerns, corporate layoffs, inflation, and persistently high interest rates. Meanwhile, on a local level, immediate disruptions like federal funding freezes, back-to-office mandates, and widespread uncertainty are creating additional stress. The result? A market where instability dominates on both fronts, leaving buyers and sellers in limbo.

The Data: Skewed, Screwed, and Largely Meaningless

Everyone loves to point to data, but let’s be clear—the numbers don’t tell us the full story. That’s because the paradigm and demographics of homebuyers have fundamentally shifted.

There are plenty of markets across the country where prices have been declining since 2022. But not in the DC metro area. In fact, as I reported earlier, prices in our market , as well as nationally, are up 6% year-over-year.

Let’s look at the numbers for the week ending January 26, 2025 (source: Bright MLS Market Report):

- Active inventory is up 21% YoY.

- Homes are taking longer to sell and experiencing more price reductions.

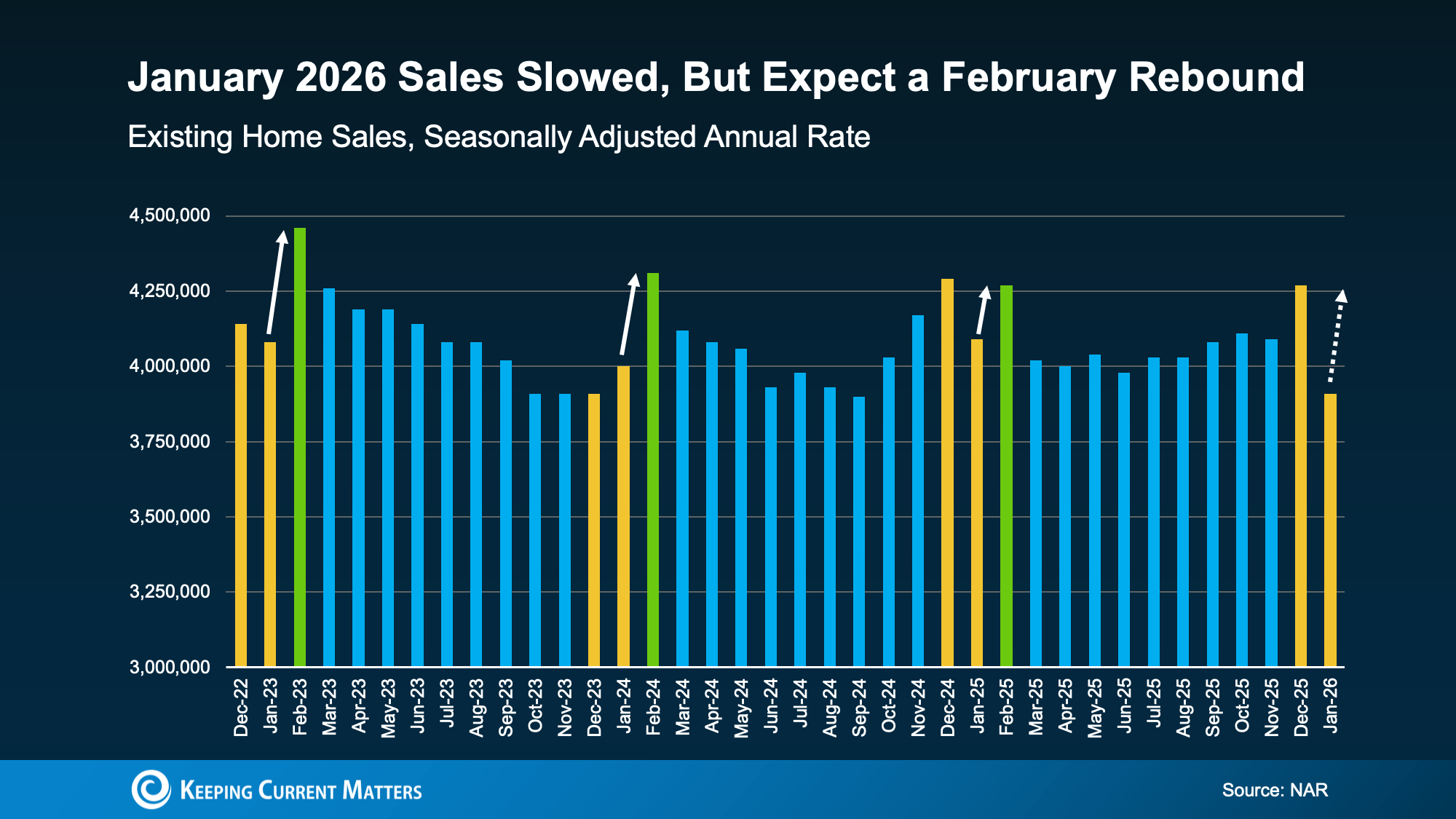

- Interest rates are hovering above 7% (source: Freddie Mac Weekly Mortgage Survey, January 2025), compared to 6% this time last year.

So, is the data helpful? Not really. These raw numbers don’t tell us much because the entire composition of homebuyers has changed.

What’s Actually Happening in the Market?

Forget the spreadsheets for a moment—let’s talk about real-world scenarios we’re seeing every day. This is from the last few weeks...

- Vienna, VA: A $1.1M single-family home had 50 showings in two days and received 9 offers over asking price.

- Hernon, VA $900,000: Dozens of showings scheduled for first day on market.

- Loudoun County: A home that sat on the market for months suddenly received multiple offers once we submitted ours.

- Laid Off Buyers canceling their home search.

- Uptick in showings across all of our active listings in all price points.

Homes lingering on the market are often overpriced, poorly presented, or facing strong competition. In contrast, well-priced homes—especially those where buyers perceive value—are selling quickly.

Today's buyers tend to come from a narrower, wealthier demographic: they are older, more experienced, and financially insulated from high mortgage rates. Unlike first-time buyers, they are less emotionally driven and more analytical, making decisions based on logic rather than urgency. They don’t feel pressured to act fast because, in their view, the next house won’t be dramatically more expensive, nor will interest rates skyrocket overnight. They feel empowered.

The hottest segment right now? Single-family homes in the $1 million range, particularly in prime locations. Anything under $1 million that is well-priced in a desirable area is commanding top dollar.

Regional Differences Are Wild

This is a bifurcated market, highly segmented by region:

- Florida and Texas for example have record-high inventory levels, leading to price declines.

- Northeast markets (including DC) continue to suffer from historic inventory shortages, driving prices up.

That’s why you’ll hear conflicting reports—prices are rising in some places and falling in others. It all depends on where and what type of home you’re looking at.

Luxury Market Boom

The high-end market is booming, or maybe it boomed already. People are calling it the "Trump Bump," where it seems like every week we are seeing record-setting sales for homes over $10 million in our region. With his new administration comes an influx of affluent political appointees, business leaders, and new members of Congress, all eager to establish residences in the nation's capital. This surge in high-end real estate activity has been unprecedented, with 87 homes selling for $5 million or more last year—a 64% increase from 2023. Half of the region's top 10 most expensive sales of 2024 closed during the tail end of December.

It's not just the ultra luxury markets, in fact nationally homes over $1M are up 44% YoY in our region, which represents a massive surge. This disproportionately pulls up median home prices, creating the illusion that all homes are appreciating when, in reality, affordability remains a major issue.

How Will the Federal Government’s Back-to-Office Mandate Impact Housing?

Some will argue that bringing government workers back to the office is great for the local market. But what I’m hearing directly from federal employees is a different story:

- They’re worried about job security.

- Childcare is a major concern.

- Taking on a higher mortgage payment isn’t even a consideration right now.

We could see some forced inventory increases if employees resign or face layoffs, needing to sell their homes. But those same individuals will turn into renters, which in turn is a positive for buyers.

So, Will Prices Come Down?

Who knows?

For now, this remains a segmented market, and buyers need to be hyper-aware of local trends rather than relying on broad national headlines.